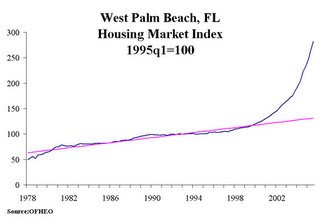

Come Back in 2015

According to this story, South Florida's high priced real estate market is closed for business for about a decade. The arrogance and greed are simply overwhelimg and out of control. Buyer's are beyond frustration.

"In the past five years, the housing crunch in South Florida has moved up the economic ladder from the low-income to the middle-class, pricing a whole new layer of workers -- thousands of Quintin Taylors -- out of the market. To live in a mid-priced house, a family in the Miami area earning the midpoint income must now spend 44 percent of its dollars on mortgage payments. That's double what it cost as recently as 1998 -- and close to Los Angeles at 46 percent and New York City at 49 percent. Even with the market slowing, South Florida still won't return to the affordable days of the late 1990s, economists say. Incomes are limited by a service and tourism economy that doesn't create enough high-paying jobs. Yet housing prices remain high because of money flowing in from foreign and investment buyers. That adds up to an affordability crunch through 2015, Moody's Economy.com forecasts. But change has come so fast that attitudes have yet to adjust. And so the quest for a home is turning into a hard lesson in compromise."

"But finding a single-family home to fit that budget won't be easy. A Florida International University study for release Wednesday found that Broward County buyers need household income of $100,000 to afford a mid-priced home. It's no better in Miami-Dade, where a Beacon Council study found that a household needs $117,204 to afford the average used single-family home."

'The renovated house, just east of Interstate 95 in Nichols Heights, is listed for $265,000, way out of Taylor's price range. But Taylor thinks he could negotiate. In 2002, the house sold for $91,500. Seven months later, it sold for $134,000. Current owner Domenick Vitale paid $160,000 for it last September. Two months later, in November, he listed it for $299,000. In December, the price dropped to $282,900. In late January, it was $265,000.

Still too high, say Lewis and Hernandez. For one thing, the house is listed as a four-bedroom, but two have no closets. ''This is really a two-bedroom with a den and a family room,'' Hernandez says. She says comparable recent sales in the neighborhood are in the $220,000 to $240,000 range. One estimate by an appraiser placed the value of the house closer to $220,000. The agents leave messages for Vitale for several days. No response. Then Hernandez leaves an urgent message that she has a buyer ready to make an offer.

Several days later, Vitale finally calls. But he's not ready to negotiate. Taylor isn't deterred. A second estimate comes in at $240,000. Taylor gets preapproval for a new mortgage with only 5 percent down and decides to make a verbal offer of $240,000. His monthly payments, with taxes and insurance included, would be $2,300 -- $650 more than he wanted to spend. ''I'll just have to cut back on things like shopping, eating out and going out to clubs every night,'' he says. ``The house is the goal.'' But there's still Vitale. The renovated house, just east of Interstate 95 in Nichols Heights, is listed for $265,000, way out of Taylor's price range. But Taylor thinks he could negotiate. The perceptions of sellers may not have caught up with the cooling market -- another factor that might keep the region unaffordable. As things slow down, sellers -- and builders -- will have to adjust, says Ned Murray, the FIU professor who directed the Broward affordability study."

Unreasonable sellers unwilling to make only 50% profit in 3 years. People making $100,000 priced out of the market. A doubling in inventory. If this is not a bubble tell me what is.

posted by BigDaddy63 @ 9:02 AM

2 comments

![]()

![]()

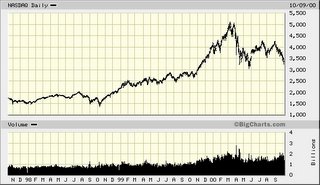

To the left is a chart from BigCharts.com that shows the NASDAQ over a 3 year period of 10/97 to 10/2000. This was during the market "bubble" and right before the proverbial fecal matter hit the fan. We all remember how it was "different this time", and how Greenspan & Co. had engineered a "new paradigm." Fundamental like earnings, sales, cash flow, were obsolete. Technical analysis was for fools. You had to buy now or pay more later for such darlings as Priceline, JDS Uniphase, and EMC.

To the left is a chart from BigCharts.com that shows the NASDAQ over a 3 year period of 10/97 to 10/2000. This was during the market "bubble" and right before the proverbial fecal matter hit the fan. We all remember how it was "different this time", and how Greenspan & Co. had engineered a "new paradigm." Fundamental like earnings, sales, cash flow, were obsolete. Technical analysis was for fools. You had to buy now or pay more later for such darlings as Priceline, JDS Uniphase, and EMC.