Where's The Reset Button?

Starting this year and going into 2007, as much as $2.5 trillion in exotic mortgages are due to be reset, as reported here story.

"You know those cheap mortgages offered to investors for speculating on housing? With somebody at the other end of a toll-free phone number offering to lend $200,000 at a monthly payment of $678 per month? Lenders who started making those teaser-rate loans a few years ago are getting ready to charge real-world payments on them. "

"The best-case scenario for the future, the one from the real estate agents, is that prices will level out to single-digit appreciation rates. Assuming that scenario, some would-be investors — those who took out highly leveraged loans with extremely low payment options — could soon find themselves owing more on a house than it’s worth. That’s called being “upside down” in a loan. "

"Many more will simply find that their monthly bill has instantly risen by roughly the amount of a car loan. The reason is that after their initial one-, two- or five-year interest, their loans are now scheduled to “reset” at more realistic rates, and will continue to do so, usually for the life of the loan."

“We don’t have enough data to know how big a problem this will be,” said David Berson, chief economist at Fannie Mae, the nation’s largest mortgage packager. "

"John Barron is typical of the new crop of homeowner-investors. They used two separate three-year, interest-only, adjustable-rate mortgages to buy the homes within the past two years. “Besides the two ARMs, we also took out a home-equity line on the Seventh Street house to put down a deposit on the Fifth Street house. There was no cash that we had in our pockets to put down on the Fifth Street house. All we had was our shining credit record — and the faith that the banks have in this real estate market that allows you to borrow 100 percent.” If they don’t sell, with interest rates rising, the couple will have to refinance the loans. "

"Barron and Wood have a lot of company, said Paul Kasriel, chief economist at Chicago-based Northern Trust. With possibly $2.5 trillion in household debt that is going to be repriced higher “the household debt-service ratio is bound to climb to new highs,” Kasriel wrote recently. Even before the reset gets under way, households were devoting a record 13.75 percent of their after-tax income to servicing debt, including mortgage debt. " “Asset bubbles are characterized by cheap credit. Usually what bursts a bubble is higher cost of credit, because that is what inflates the bubble: cheap credit,” he said. "

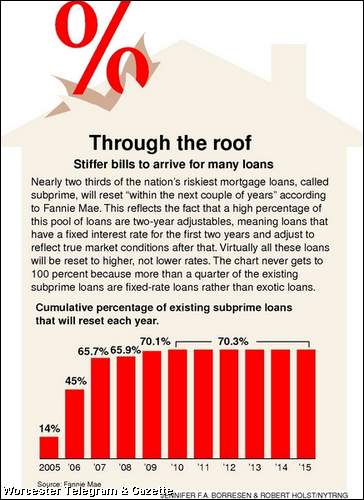

"Fannie Mae looked at 2002-2004 loan data to determine what portion of the existing loan pool would be “adjusted,” and when. Fewer than 10 percent of the conventional conforming loans will reset in 2006-2007, but nearly two-thirds of sub-prime loans will.

“The estimate is that in 2007, more than a trillion dollars’ worth of hybrids are going to hit their first reset date,” he said. That one chunk of hybrid loans represents 12 percent of the $8.8 trillion in single-family home loans outstanding nationwide. "

This is the calm before the storm folks. Remember the phrase being "upside down" in a loan. You will be hearing alot of that in the years to come. Couple the explosion in listings with the soon to be increase in payments, and the soon to come mad dash to the exits will be bloody.

posted by BigDaddy63 @ 7:15 PM

0 comments

![]()

![]()

0 Comments:

Post a Comment

<< Home